Trading for retirement is a conversation the financial services industry rarely starts and almost never finishes honestly. Instead, retirement planning follows a well-worn script: contribute to a pension fund, buy unit trusts, diversify into property, accept a 3.9% annual safe withdrawal rate in your sixties, and hope the numbers hold up for twenty or thirty years of post-retirement life.

For the estimated 94% of South Africans who cannot retire comfortably on that model alone, and for the growing global cohort of professionals who have quietly run the numbers and realised the traditional approach will not sustain the life they have worked four decades to build, this article offers something different.

Not a get-rich shortcut, not a speculative alternative to traditional savings, and not retirement, and or investment advice. A structured, governance-based income framework – built on the same business principles that serious professionals already use – that positions trading as a legitimate, managed component of a retirement income strategy.

The Retirement Income Crisis Nobody Is Talking About Plainly

Here are the numbers – unvarnished.

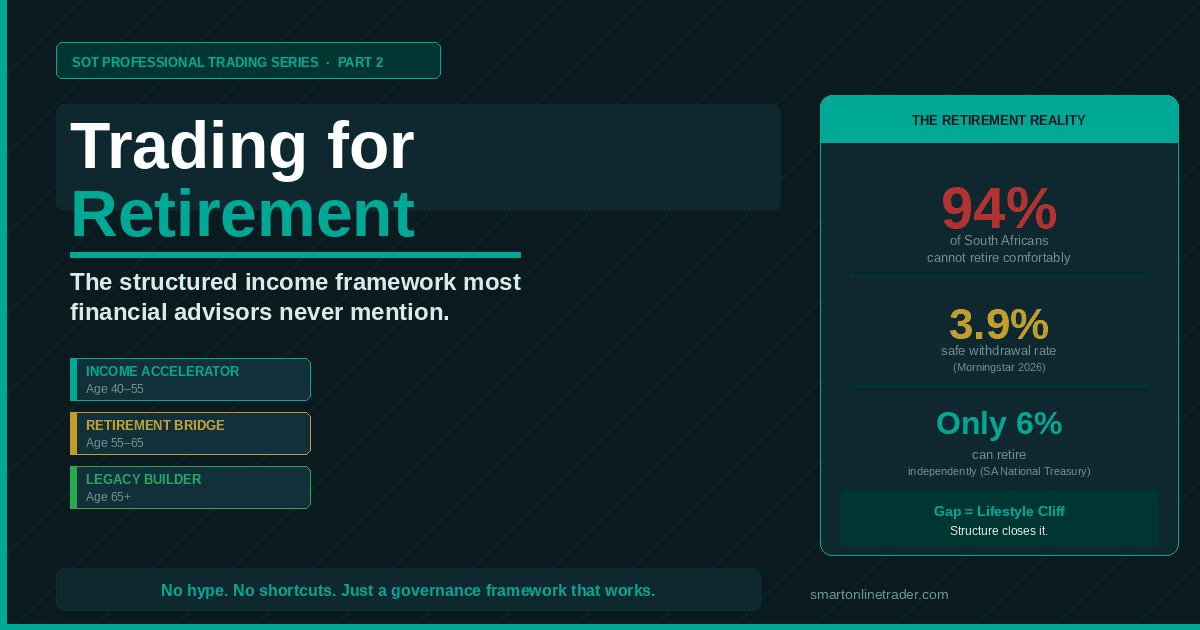

South Africa is facing a retirement crisis, with estimated 94% of the population not able to retire comfortably. Only 6% of South Africans can retire independently, according to National Treasury data. Of the 5.2 million South Africans aged 60 and older, 73% are recipients of social grants, and 2% of retirees confirmed they had already run out of funds entirely and are relying on state or family support. MFS + 2

These are not fringe statistics. They represent the lived reality of the majority. And they are not uniquely South African.

Globally, 28% of first-wave Gen X respondents aged 55 to 60 said they are extremely or very concerned about having enough income to last their lifetime – double the rate of Boomers. Nearly half of Gen Xers surveyed anticipated returning to work after retirement due to financial concerns, compared with only 21% of Boomers.

Among consumers with between $250,000 and $2 million in investable assets, 38% do not have a specific retirement income plan – meaning even the relatively affluent are navigating retirement without a defined strategy. IQ Hashtags + 2

The conventional solution – save more, diversify more, spend less in retirement – is mathematically insufficient for most people. Morningstar’s current base-case safe withdrawal rate for a new retiree planning a 30-year retirement horizon is 3.9%.This means a R5 million portfolio generates approximately R195,000 per year before tax. For a professional accustomed to a salary of R600,000 to R800,000 annually, that gap is not a rounding error. It is a lifestyle cliff. Display Purposes

The question is not whether to find additional income sources in retirement. For the vast majority, there is no choice. The question is which additional income sources are structured, sustainable, and consistent with the risk profile of someone who no longer has a primary salary as a backstop.

Why Trading Is Not What Retirees – or Pre-Retirees – Think It Is

The moment trading enters a retirement conversation, one of two reactions typically follows. Either the person shuts it down entirely – “that is gambling, not retirement planning” – or they lean into it recklessly – “I can day-trade my way to an income.” Both reactions miss the point entirely. And both stem from the same misunderstanding: that trading is a single, undifferentiated activity.

It is not. The word “trading” covers a spectrum of approaches that range from irresponsible speculation to systematic, governance-driven income generation. The speculative end of that spectrum – instinct-based, reactionary, undisciplined – is what most people picture. It is also what produces the 75 to 90% evaluation failure rate in the prop firm industry, and what destroys retail accounts in concentrated bursts.

The other end of the spectrum – structured, process-documented, risk-defined, consistently measurable – is what this article is about. It is the same end of the spectrum addressed in the second business trading framework. The only difference is the context in which it is deployed.

For a pre-retiree aged 45 to 60 with an existing capital base, a stable income, and a ten to fifteen year runway before full retirement, the structured trading model offers something no traditional retirement product does: an active, scalable income stream with defined downside, minimal correlation to traditional asset classes, and the ability to generate returns in both rising and falling markets.

That is not a speculative claim. It is the structural mathematics of a well-governed trading operation, applied to the specific context of retirement income planning.

The South African Retirement Landscape in 2026 – Context Matters

South Africa’s retirement environment has undergone significant structural changes in the past 24 months that make this conversation more urgent – and more relevant – than at any previous point.

South Africa has officially moved away from the traditional default retirement age of 60, with new pension regulations taking effect from January 2026, reshaping retirement planning for millions of workers.

The fixed benchmark that an entire generation planned around no longer exists as a structural anchor. Retirement is now a personal inflection point rather than a mandated milestone – which means the planning responsibility has shifted fully to the individual. Morningstar

Simultaneously, South Africa’s Two-Pot retirement system, which took effect in September 2024, has created a hybrid model that demands a much higher level of financial literacy from the average member.

The system divides contributions into a savings pot and a preservation pot – and in the first week of March 2026 alone, coinciding with the new tax-year withdrawal window, more than 30,500 claim requests were submitted, the majority for emergency expenses rather than strategic financial planning. T. Rowe PriceICI

Old Mutual cautions that improved preservation should not be confused with retirement adequacy – preservation alone will not solve the country’s retirement crisis if workers are not contributing enough in the first place. BlackRock

What all of this means practically: the traditional retirement system, even with its recent reforms, was never designed to produce retirement income adequacy for professionals with mid-to-high income expectations. It was designed to prevent complete destitution. Those are two very different objectives. The gap between them is where structured trading has a legitimate, specific, and powerful role to play.

The Trading for Retirement Framework – Three Distinct Roles

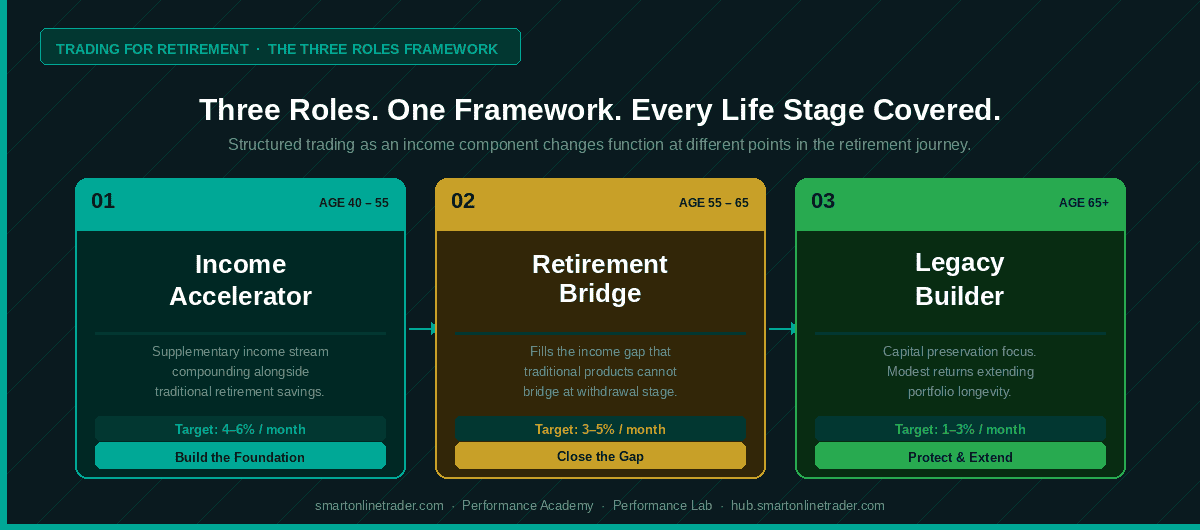

Trading does not replace traditional retirement savings in this framework. It augments, accelerates, and extends them. There are three specific roles it plays, depending on the individual’s life stage and capital position.

Role 1: The Income Accelerator (Age 40 to 55, Still in Employment)

For the professional in their prime earning years with disposable income and a ten to fifteen year runway to retirement, structured trading could function as a potential income accelerator. The objective is not to replace the primary salary – it is to generate an additional income stream that compounds alongside traditional retirement savings, shortening the savings window or expanding the capital base available at retirement.

In practical terms: a disciplined trader operating within a prop firm funded model with a $100,000 simulated account generating a consistent 4% to 6% monthly return – conservative by funded trader standards – is producing $4,000 to $6,000 per month in supplementary income. Compounded over ten years alongside a conventional retirement fund contribution, the impact on retirement capital is transformative.

The critical governance requirement at this stage is that trading income is treated as supplementary, not primary. The emotional pressure of needing the trading income to pay bills introduces exactly the conditions – psychological pressure, decision-making under financial stress – that undermine process compliance. Income acceleration works because the primary income removes that pressure entirely.

Role 2: The Retirement Bridge (Age 55 to 65, Transitioning Out of Employment)

For the professional transitioning out of full-time employment, structured trading may fill the income gap that traditional retirement products cannot bridge. 51% of South African retirees are not able to make ends meet, largely because the withdrawal rate required to sustain their lifestyle exceeds what their capital base can safely support long-term. Halter Ferguson

A structured trading operation producing consistent monthly income of 3% to 5% on a defined capital allocation – with strict maximum drawdown protocols – addresses this gap without eroding the principal retirement capital.

The trading capital is ring-fenced, governed by the same drawdown protocols as any other structured financial operation, and contributes a defined monthly income to the overall retirement income stack.

This is not passive income in the traditional sense. It requires active, disciplined session management. But for a recently retired professional with time, analytical capability, and a structured framework, it is both achievable and realistic – particularly within the SOT ecosystem where the governance infrastructure, expert mentoring, and community accountability are built into the model.

Role 3: The Legacy Builder (Age 65+, Capital Preservation Focus)

For the retiree who has established a funded trading track record over the preceding decade, the model shifts from income generation to capital preservation and selective compounding. Trading frequency reduces. Position sizes reduce. The governance framework tightens further.

The objective is no longer to generate maximum monthly income – it is to protect the capital base while generating modest, consistent returns that extend the longevity of the retirement portfolio significantly beyond what a passive withdrawal strategy alone would achieve.

At this stage, sequence of returns risk – the possibility of a market downturn in the early years of retirement permanently reducing what a portfolio can support – is the primary concern. A governed trading operation that can generate positive returns in both rising and falling markets directly mitigates this risk in a way that traditional equity or bond portfolios cannot. IQ Hashtags

The Five Numbers Every Pre-Retiree Should Know

Before any trading-for-retirement framework makes sense, the individual needs clarity on five financial numbers. These are not trading numbers. They are retirement planning numbers – and without them, no trading strategy can be calibrated correctly.

Your replacement ratio target. The widely accepted planning benchmark is replacing 75% to 80% of your pre-retirement income in retirement. Calculate your current gross monthly income and multiply by 0.8. That number potentially indicates your monthly retirement income target. Write it down.

Your capital adequacy gap. Based on your current retirement savings trajectory, calculate the projected capital base you will have at your intended retirement date. Apply the 3.9% Morningstar safe withdrawal rate. The difference between that annual income figure and your replacement ratio target is your capital adequacy gap. For most professionals, this gap is significant – and it is the number that defines how much additional income the trading component needs to contribute.

Your trading capital allocation. Trading capital should never exceed 10% to 15% of total investable assets at the income-acceleration stage, reducing to 5% to 10% as you move into the retirement bridge phase. This is the ring-fenced allocation – money that can sustain a defined drawdown without affecting lifestyle or primary retirement capital.

Your maximum monthly drawdown tolerance. This is the most important number in the trading governance framework. Define, in rands, the maximum monthly loss on your trading capital that would have zero impact on your retirement plan. This number – not your potential profit – defines your position sizing, your daily loss limits, and your evaluation parameters.

Your income target from trading. Based on your capital adequacy gap and your trading capital allocation, calculate a realistic monthly income target for your trading operation. A conservative, governance-compliant target of 3% to 5% monthly on trading capital could be achievable within the structured framework. An aggressive, unrealistic target is the first sign that the trading component is being asked to carry a weight it was not designed to bear.

Why the Prop Firm Model Is Particularly Suited to Retirement Income Planning

One of the most common objections to trading as a retirement income component is capital exposure – the concern that trading requires putting retirement savings at risk. The prop firm evaluation model directly addresses this concern in a way that most people are not aware of.

The Performance Lab simulated funded account model allows a trader who has demonstrated consistent, governance-compliant performance to access trading capital that is not their own. A $100,000 simulated funded account requires an evaluation fee – not $100,000 of personal capital. The “profits” generated on that simulated funded account are shared with the trader according to the payout structure. The personal retirement capital is never at risk beyond the evaluation fee.

This is structurally identical to the capital access model described in the second business trading framework: demonstrated performance earns proportionate simulated capital access. For a pre-retiree building a trading track record over a ten to fifteen year runway, this means that by the time retirement approaches, the trading income component is being generated on capital that is not drawn from the retirement pot at all. The retirement capital grows undisturbed. The trading income adds to it.

The prerequisite – and this cannot be overstated – is that the governance infrastructure is in place before any evaluation is attempted. The Performance Academy provides that infrastructure in a structured, mentored curriculum that is specifically designed to be completed alongside a full-time career. The Performance Lab evaluation is the milestone that marks the transition from preparation to a simulated funded operation.

The Honest Conversation About Risk

Any retirement income framework that avoids the risk conversation is not a framework – it is a sales pitch. Here is the honest version.

Structured trading carries risk. Even with robust governance, defined stop-losses, written drawdown protocols, and expert mentoring, there will be losing sessions, losing weeks, and occasionally losing months. The trading component of a retirement income strategy will not produce a perfectly linear return curve. At best, few financial instrument does.

What the governance framework controls is the magnitude and duration of drawdowns. A trader operating within a defined maximum daily loss, a tiered drawdown protocol, and a 1% to 2% risk per trade framework does not experience catastrophic losses. The losses are bounded, documented, and recoverable. The difference between a managed drawdown and an account-blowing loss is entirely structural – not a matter of market conditions or trading strategy.

The honest question is not whether trading involves risk. Everything in a retirement portfolio involves risk. The honest question is whether the risk is defined, managed, and proportionate to the potential return. For a governed trading operation within the SOT framework, the answer is yes – provided the governance infrastructure is built correctly before capital is deployed.

The SOT Trade Readiness Checklist is the starting point for that assessment. Seven items. If you cannot tick all seven with documented evidence behind each one, the governance infrastructure is not yet in place. Build it first. Deploy capital second and always consult your licensed Broker or FSP.

Who This Model Works For – and the Honest Disqualifiers

The trading-for-retirement framework is not universally appropriate. Here is the honest qualification.

It works well for professionals who have a stable primary income that removes financial pressure from trading decisions, a ten to fifteen year runway before retirement ideally, an existing familiarity with financial risk frameworks, the analytical capacity to work within a structured, documented process, and a genuine willingness to build the governance infrastructure before generating income.

It is genuinely not suited to individuals who need immediate income from the trading component, who are unwilling to document their process rigorously, who are approaching retirement within two to three years without an existing trading track record, or who are drawn to the model primarily by the income potential rather than the structural discipline it requires.

The Capital Clarity Call with the SOT team is the appropriate starting point for anyone unsure which category they fall into. It is a focused, no-pressure diagnostic conversation – not a sales call – not financial- and or investment advoce – that maps your risk profile and trade readiness against the SOT pathway that makes sense for your situation. Book it at smartonlinetrader.com/.

Your Next Step – A Three-Stage Entry Into the Framework

Regardless of your age or current financial position, the entry path into the trading-for-retirement framework follows the same three-stage sequence.

Stage 1: Diagnose your position. Use the SOT Trade Readiness Checklist to audit your current governance infrastructure. Then chat to Siya at present.smartonlinetrader.com – the SOT AI Success Profiler – to map your checklist score to the specific SOT pathway that matches your starting point.

Stage 2: Build the foundation. Enrol in the Performance Academy pathway that matches your assessment. The curriculum is structured around the governance competencies that simulated funded traders demonstrate – not generic technical trading content. It is designed to be completed alongside a full-time career, with expert mentoring from *Francois du Plessis (FSP · FCSA Category 2, under supervision) and Luhan Oosthuizen (Senior Analyst · Prop Firm Trader expert) delivered through the SOT Community Hub.

Stage 3: Access capital proportionate to your track record. When your documented performance demonstrates evaluation readiness – 30 to 60 days of consistent, governance-compliant trading – register for your Performance Lab challenge. Pass it, and your trading income component begins generating on capital that is not drawn from your retirement savings.

The runway to retirement is not infinite. The best time to start building the governance framework was ten years ago. The second best time is today.

Frequently Asked Questions About Trading for Retirement

Is trading for retirement income realistic or is it a fantasy?

It is realistic under specific conditions – and a fantasy under others. The conditions that make it realistic: a stable primary income removing financial pressure from trading decisions, a structured governance framework in place before capital is deployed, a realistic income target calibrated to a conservative monthly return on trading capital, and a minimum five to ten year development runway. The conditions that make it a fantasy: treating it as a get-rich shortcut, operating without documented governance, chasing unrealistic monthly return targets, or deploying retirement capital before a funded track record has been established.

How much capital do I need to start?

Less than most people assume. The Performance Academy enrolment is the primary initial investment – no trading capital is required during the foundation phase. The Performance Lab evaluation fee is the entry point to simulated funded capital access, not the capital itself. Your personal retirement savings remain untouched during both phases. Only if you choose to run a personal live account in addition to a funded account does personal trading capital become relevant – and even then, the maximum allocation should never exceed 10% to 15% of total investable assets.

How does this fit with South Africa’s Two-Pot retirement system?

The Two-Pot system governs contributions made to a registered retirement fund and is a separate vehicle entirely from a trading income strategy. The trading component described in this article is an additional income stream – not a withdrawal from or replacement of the Two-Pot structure. The Two-Pot preservation pot continues undisturbed. The trading income could add to total retirement wealth independently, and could reduce the pressure to withdraw from the savings pot for emergency expenses by providing an alternative liquidity source.

I am 55 years old. Is it too late to start?

It depends on your honest assessment of two factors: your current governance readiness and your retirement timeline. A 55-year-old with ten years to retirement, a stable income, and the analytical capability to build a governance framework within twelve to eighteen months has a viable entry path. A 55-year-old with five years to retirement and no existing trading infrastructure needs a more conservative entry point – potentially the retirement bridge role described above, with a smaller capital allocation and more conservative income targets. I recommend having a Capital Clarity Call with your licensed Broker and or FSP to get specialised answers to this question for your specific situation.

What is the SOT Community Hub and how does it support retirement planning?

The SOT Community Hub is the accountability and mentoring layer of the SOT ecosystem – and access is completely complimentary. Inside the Hub, *Francois du Plessis (FSP · FCSA Category 2, under supervision) and Luhan Oosthuizen (Senior Analyst · Prop Firm Trader) post market insights and trade analysis. The Hub provides the peer accountability, expert oversight, structured education and a community that solo self-study cannot replicate. The Hub and the content are not for investment- and or retirement planning and or advice – but offers a professional network for prop trading education. The aim is to educate and mentor you progress from a novos to simulated funding with clear rules and accountability.

How does this article relate to the Second Business Trading framework?

This article is Part 2 of the SOT Professional Trading Series. The Second Business Trading article established the five business principles and the governance framework that applies to all structured trading operations. This article applies that same framework specifically to the retirement income context – the three roles trading plays at different life stages, the five numbers every pre-retiree needs to calculate, and the honest risk conversation that retirement planning advice from a licensed Broker or FSP must include. Both articles are built on the same Blue Ocean premise: structure, not speculation, is what makes trading a legitimate professional income stream.

Find out where you stand and which pathway matches your retirement timeline.

Join the community and download your SOT Trade Readiness Checklist

Ready to start and progress to your simulated funded trading track record?

*IMPORTANT NOTICE and DISCLAIMER

Smart Online Trader SA, and its employees are not licensed Financial Services Providers (FSPs) and do not provide financial, investment, or retirement planning advice. The content of this article is intended for educational and informational purposes only and does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instrument.

Online trading and prop firm trading involves substantial risk of loss and is not suitable for all individuals. Past performance is not indicative of future results. You may lose some or all of your capital.

Never trade with money you cannot afford to lose.

Smart Online Trader SA specialises exclusively in online trading education and prop firm evaluation preparation. Before making any investment or trading decision, always consult a licensed Financial Services Provider, a qualified financial advisor, or your registered broker who can assess your personal financial circumstances, risk tolerance, and investment objectives.

*Mr. Francois du Plessis operates as an Authorised Representative under supervision of AT Global Markets SA (Pty) Ltd, an Authorised Financial Services Provider, FSP No. 44816, Registration No. 2013/129459/07. This representative capacity and any consulting services rendered thereunder do not constitute financial advice on behalf of Smart Online Trader or any of its business units.